Most P&C insurance products are built around the same fundamental premise: something bad happens, a loss is assessed, and a check is written. That model has served the industry well for over a century. But it has limits, and they are becoming more visible as climate volatility increases, global supply chains grow more fragile, and underserved markets demand coverage that traditional indemnity structures can’t efficiently deliver.

Parametric insurance doesn’t replace indemnity. But it solves problems that indemnity can’t. For P&C carriers willing to invest in the capability, it opens the door to market segments, risk categories, and client relationships that are otherwise out of reach.

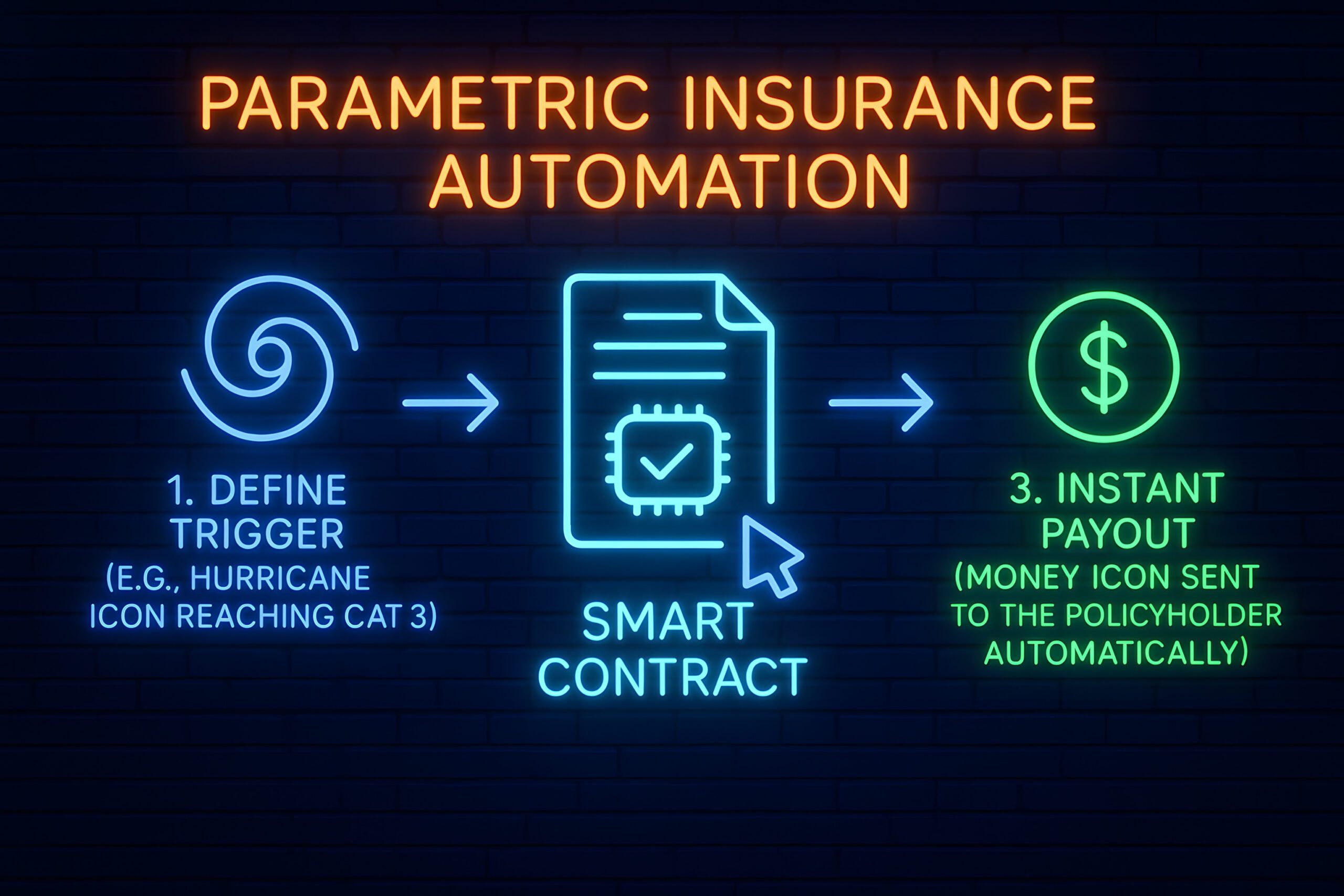

1. What is Parametric Insurance?

Parametric insurance pays a predetermined amount when a defined triggering event occurs regardless of the insured’s actual measured loss. The payout is tied to an objective parameter: wind speed at landfall, earthquake magnitude, rainfall levels at a specific gauge, a market index, a flight delay, or any other measurable variable that correlates with loss.

There is no claims adjuster. No loss assessment. No lengthy investigation. If the trigger is hit, the policy pays.

This distinction has profound implications for both the economics of insurance and the experience of being insured. Indemnity insurance is designed to make a policyholder whole. Parametric insurance is designed to deliver liquidity quickly, predictably, and transparently.

A simple example: a regional hotel chain on the Gulf Coast purchases a parametric wind policy with a trigger of Category 3 hurricane making landfall within 50 miles of their properties. When that event occurs, they receive a fixed payout within days, even if their actual structural damage is less than the payout, or more. The speed and certainty of the cash is the product.

Where Parametric Insurance Solutions are Used Today

Parametric structures have been used in specialty and reinsurance markets for decades. Their application at the carrier level has expanded significantly in recent years, particularly in:

Natural Catastrophe

Hurricane, earthquake, and flood parametric products are well-established, particularly for commercial property and infrastructure owners in exposed geographies. The World Bank has used parametric structures to provide rapid sovereign disaster relief; private carriers have adapted the model for middle-market commercial clients.

Agriculture

Index-based crop insurance tied to rainfall or temperature data has expanded access to coverage for smallholder farmers globally. In the U.S., USDA programs include parametric elements. Agribusiness carriers have developed increasingly sophisticated trigger structures tied to satellite and IoT sensor data.

Travel and Aviation

Flight delay products that pay automatically when a departure delay exceeds a threshold are one of the most consumer-visible applications. Carriers like Allianz and Cover Genius have built significant travel parametric books. The low-friction claims experience has driven strong retention.

Marine and Cargo

Port congestion indices and voyage delay triggers are being used to supplement traditional marine cargo coverage, particularly for clients with high supply chain sensitivity and cash-flow exposure from delays.

Where the P&C Insurance Market is Moving in 2026

The frontier of parametric insurance is no longer natural catastrophe. Carriers and MGAs are pushing into:

• Cyber resilience triggers tied to outage duration or sector-wide incident indices

• Supply chain disruption coverage based on shipping index data or named port closure events

• Renewable energy output shortfalls tied to wind speed or solar irradiance data

• Construction delay products triggered by adverse weather thresholds during a project window

• Political risk and trade sanctions tied to government-issued event declarations

The common thread: Each of these risks has historically been difficult or expensive to underwrite on an indemnity basis because loss assessment is slow, contested, or administratively burdensome. Parametric structures sidestep the assessment problem entirely.

The Underwriting Challenge: Basis Risk

No discussion of parametric insurance is complete without an honest accounting of its central limitation: basis risk.

Basis risk is the gap between what the trigger measures and what the insured actually experiences. A hotel on the Gulf Coast might hold a parametric wind policy that triggers at 100 mph sustained winds at the nearest official measurement station, but if the storm tracks slightly north, the station records 98 mph while the hotel sustains significant damage. The policy doesn’t pay.

The inverse is also true. A policy might pay out when the insured suffered no meaningful loss — a financial benefit, but one that can complicate regulatory and accounting treatment. Basis risk is not a reason to avoid parametric structures. It’s a design problem to be solved. The carriers building durable parametric books are investing in the analytical infrastructure to minimize it.

The underwriting imperative: Design triggers that are tightly correlated with actual client exposure. This requires rigorous data analysis, granular location modeling, and in many cases, a willingness to use non-standard data sources including satellite imagery, IoT sensors, and third-party indices.

Why Carriers Should be Building This Capability Now

There are several compelling reasons for P&C carriers to develop parametric underwriting capability, beyond simple market expansion:

1. Profitable access to underinsured markets. Many segments (i.e., small agribusinesses, municipalities, infrastructure operators in emerging markets) represent genuine insurance need but are economically unviable to serve with traditional indemnity products due to high adjustment costs relative to premium. Parametric structures change the unit economics entirely.

2. Lower claims handling costs. Eliminating loss adjustment expense (LAE) from parametric lines is structurally significant. For cat-exposed books, LAE can be a substantial component of combined ratio. A parametric product that triggers automatically has near-zero LAE, improving margin even at competitive premium levels.

3. Superior client experience and retention. Clients who receive a payment within 72 hours of a hurricane landfall, before they’ve even filed a traditional claim, remember that experience. In an industry where switching barriers are largely price-driven, delivering meaningful value at the moment of loss is a powerful retention mechanism.

4. Reinsurance and capital efficiency. Parametric structures are highly reinsurable. Cat bonds, ILS capacity, and traditional reinsurers have deep familiarity with parametric triggers. Carriers with well-structured parametric books can access efficient reinsurance capacity and, in some cases, transfer risk to capital markets directly.

5. Competitive differentiation. In a softening market where most carriers are competing on price for the same risks, parametric capability is a genuine differentiator. It allows carriers to offer products that competitors simply cannot, protecting margin and building broker relationships that go beyond price.

How Carriers Can Begin Shifting Toward Parametric Insurance

Developing parametric capability doesn’t require a wholesale transformation of a carrier’s book. The most effective approaches start focused and scale deliberately.

Start with a line you already know.

The best entry point for most carriers is a commercial line where they already have exposure data and loss history. A carrier with a strong coastal property book, for example, already understands the risk. The task is designing a parametric structure that complements or supplements existing indemnity coverage. This reduces data uncertainty and allows underwriters to validate trigger design against known experience.

Invest in trigger design and data partnerships.

Parametric underwriting is fundamentally a data discipline. Carriers need reliable, third-party data sources for triggers (i.e., NOAA weather data, USGS seismic data, shipping indices, energy output data) and the analytical infrastructure to model the correlation between trigger events and actual client losses. This often means building data partnerships that don’t exist in traditional underwriting workflows.

Align product design with client communication.

Basis risk is not just an underwriting problem, it’s a client relationship problem. Policyholders accustomed to indemnity insurance may be surprised when a parametric policy pays out less (or more) than their actual loss. Carriers that succeed with parametric products invest in clear policyholder education, transparent trigger documentation, and honest conversations about what the product is and isn’t designed to do.

Build the systems infrastructure to support automated payouts.

The operational promise of parametric insurance requires systems that can monitor trigger data feeds, execute payout calculations, and initiate disbursements without manual intervention. This is a materially different workflow from traditional claims handling. Carriers with modern, API-connected policy administration systems are far better positioned to build this infrastructure than those relying on legacy platforms.

Consider MGA partnerships as a low-risk entry point.

Several MGAs have already built sophisticated parametric underwriting capabilities. Carriers looking to enter the market without building full internal capability can partner with or provide capacity to these MGAs gaining exposure to the risk class, learning from experienced parametric underwriters, and evaluating the economics before committing to a larger internal build.

The Bottome Line on Parametric Insurance

Parametric insurance isn’t a niche product or a future-state innovation. It’s a structurally different approach to risk transfer that is already demonstrating its value across multiple lines and geographies, and its footprint is expanding.

For P&C carriers, the question isn’t whether parametric structures will become more prevalent. They will. The question is whether your organization will develop the data capabilities, product design expertise, and systems infrastructure to participate, or whether you’ll watch competitors and MGAs capture those market opportunities instead.

The carriers that begin building parametric capability now will accumulate the data, experience, and infrastructure that make scaling this capability progressively easier. Those that wait will find the learning curve considerably steeper.

About WaterStreet

WaterStreet Company is a trusted technology and service partner to property and casualty insurers, MGAs, and insurtechs. Founded in 2000 and headquartered in Kalispell, Montana, WaterStreet delivers a comprehensive suite of solutions that combine modern policy administration software with U.S.-based back-office services to help carriers scale efficiently.

Reach out to WaterStreet Company today to request a consultation and demo.